HSAs Skimmed

Take it to the limit

Employees who decide to enroll in the company’s high-deductible health insurance plan (HDHP) can qualify for an HSA. This helps to offset the cost of their HDHP, and give them some tax benefits in the process.

For 2026, the IRS has set (for an individual) an HSA contribution limit of up to $4,400 or up to $8,750 for family coverage. For anyone 55 or older anytime this year, they will be able to contribute an extra $1,000.

For 2027, the IRS has increased the HSA contribution limits to $4,500 for individuals and $9,000 for family coverage. Individuals age 55 and older can continue to make an additional $1,000 catch-up contribution, bringing their total contribution opportunity to $5,500 for self-only coverage or $10,000 for family coverage.

It’s important for your employees to know exactly what is covered by their HSA, because they will be responsible for verifying the eligibility of purchases themselves. A lot is covered, so sometimes it is easy to make assumptions. For example, gym memberships, while health-related, are not covered.

Want to see more of what’s covered? Here is a list of what is covered.

Using your FSA or HSA should feel simple, not stressful.

With Care Covered, Ameriflex participants now have a clear destination to shop for eligible products, confidence that purchases will qualify, and peace of mind knowing the experience is backed by the same standards they already trust.

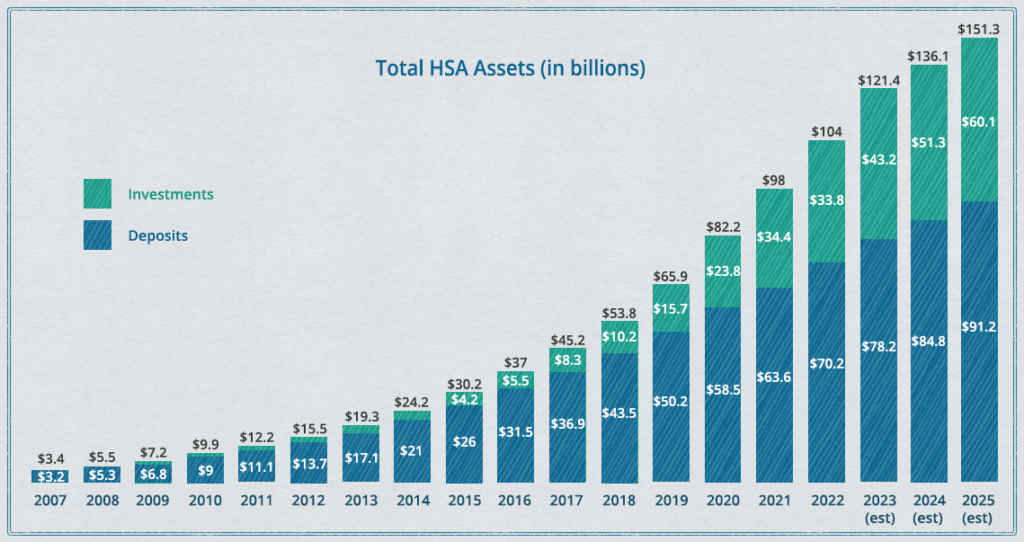

As HSA offerings become more and more common, top tier talent is coming to expect benefits such as an HSA plan from their employer. HSA research firm Devenir found that health savings accounts grew to over 36 million accounts in 2023, and those accounts held $116 billion in assets — a 17% increase over the year before.

Why are HSAs on the rise? Simply put, it’s a competitive economic environment. In light of the pandemic, employers are having to do more in order to attract talent, and to keep the talent they have. This isn’t a short-term trend, either — Devenir projects that the HSA market will exceed 40 million accounts by the end of 2025, holding over $150 billion in assets.