Flexible Spending Account (FSA)

Set aside tax-free money for health expenses

Overview & Eligibility

2026

Contribution Limit: $3,400

This is the maximum amount that can be contributed to an FSA each year per the IRS.

Carryover: $680

The Value for Employees

Employees can save up to 40% on thousands of eligible everyday expenses such as prescriptions, doctor’s visits, dental services, glasses, over-the-counter medicines, and copays.

Every dollar an employee contributes to an FSA lowers their taxable income. Let’s say an employee earns $40,000 a year and contributes $1,500 to an FSA. That means only $38,500 of their income gets taxed.

Employees will receive an Ameriflex Debit Mastercard® linked to their FSA. Employees can use their card for eligible purchases everywhere Mastercard® is accepted. Account information can be securely accessed 24/7 online and through the mobile app.

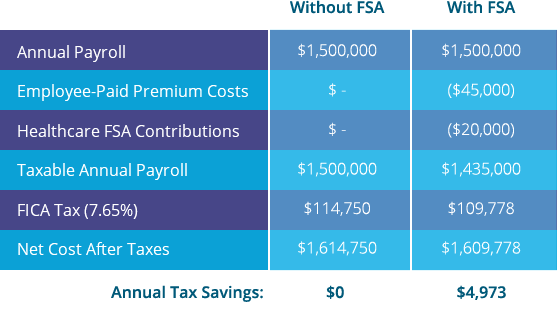

The Value for Employers

Since contributions to FSAs are taken out pre-tax, no payroll taxes are due on the amounts employees contribute to the FSA.

Nearly one-fourth of U.S. adults say they have problems paying medical bills. Helping employees save money on their everyday medical expenses can aid in employee retention and recruitment.

Healthcare is complicated. The Ameriflex Client Relationship Team is eager to answer questions and provide assistance. Our Net Promoter Score (NPS) far exceeds the healthcare average.